The IRS needs to make changes to its management controls for overseeing revenue officer case actions, the Treasury Inspector General for Tax Administration found in its latest report.

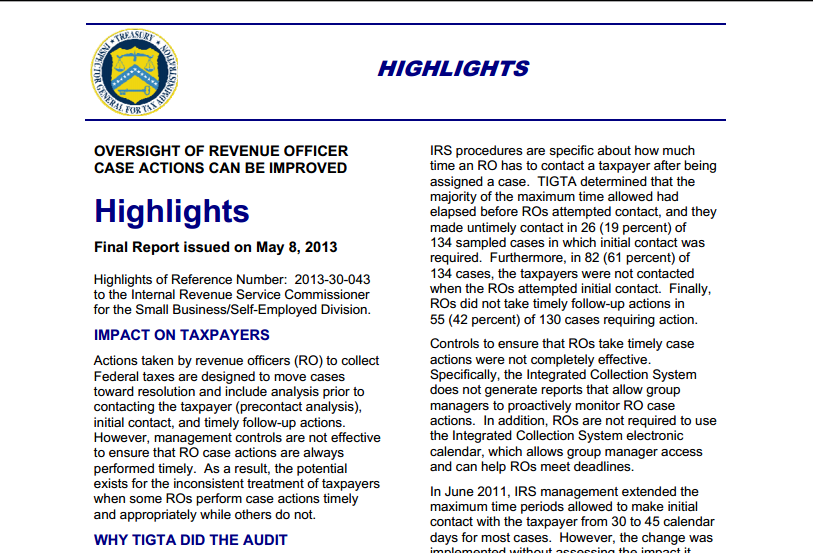

The report looked at 139 cases closed by revenue officers in the Small Business/Self-Employed Division Collection Field function and found inconsistencies in how ROs handled them. In 44 percent of the cases reviewed, ROs failed to perform an analysis or take follow-up actions in a timely manner.

“When some revenue officers perform case actions timely and appropriately while others do not, the potential exists for inconsistent treatment of taxpayers and ineffective collection of revenues,” said J. Russell George, the Treasury Inspector General for Tax Administration. “The more time that passes before taxpayers make at least one payment, it becomes less likely that they will do so at a later date. Meanwhile, taxpayers who are not contacted timely may accrue more interest and penalties compared with taxpayers who are promptly contacted.”

The current IRS procedures require ROs to conduct an analysis before making initial contact with a taxpayer, but it does not specify a timeframe in which the analysis is to be completed. It does, however, outline how much time ROs have to contact a taxpayer after being assigned a case. TIGTA’s review found that in 6 percent of the cases, the required analysis was either not completed or completed after the RO contacted the tax payers. In addition, ROs made untimely contact in 19 percent of the cases requiring initial contact and did not follow up in a timely manner in 55 percent of the cases requiring follow-up actions.

In June 2011, IRS management increased the maximum time allowed for initial contacts without assessing the impact on inventory, workload or revenue. TIGTA’s audit report found that management controls currently in place were ineffective and suggested that management evaluate the impact of the previous procedural change. TIGTA also made several suggestions for improving the timeliness of RO case actions.

IRS management agreed with most of TIGTA’s recommendations and plans to take corrective action. However, they did not agree that additional controls were necessary for ensuring analyses were performed before making initial contact with taxpayers. Though, management did agree to remind ROs.

Thanks for reading CPA Practice Advisor!

Subscribe Already registered? Log In

Need more information? Read the FAQs

Tags: IRS